The YieldMax Trap: Why Massive Dividends Can Make You Poorer

Breaking Down NAV Erosion, Taxes, Fees, and the Illusion of Free Money with TSLY, AMZY, CONY, and More!

Over the last several years, the concept of dividend investing has spiked in interest. The idea of getting passive income for just holding onto stocks, having those payouts grow over time, and eventually having those payouts cover your rent, bills, etc. sounds like a dream. And to an extent, it can be achievable.

With the rise of interest in dividend payers, companies like ZEGA Financial/YieldMax and other money managers have introduced products that pay out high-yield “dividends” frequently. Some pay monthly, some pay weekly, and some pay every two weeks. And while this sounds amazing, there unfortunately is a darker side to this that most do not realize.

What are These Products?

Unfortunately, many online investors market these products as actual dividends from a company’s profits. Some investors even go as far as saying these products are “free money.”

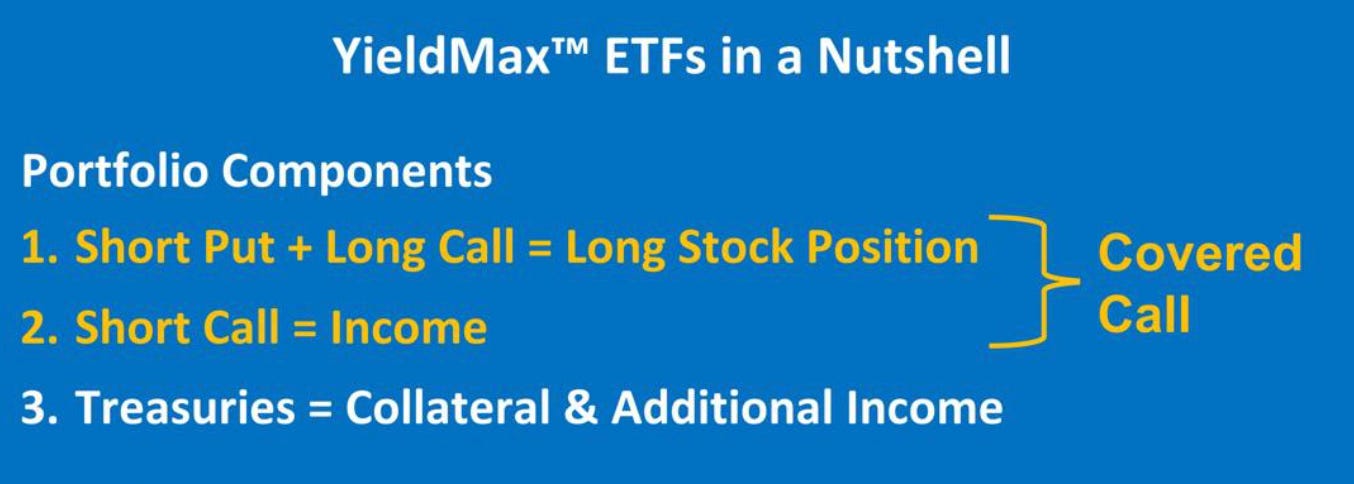

These ETFs generate high income using options contracts instead of buying actual stocks. They mimic a target stock’s price movements and sell call options to collect cash premiums.

These continuous premiums fund the fund’s massive monthly/weekly payouts to investors. However, your upside profit is strictly capped, while your downside risk remains completely unlimited.

Unfortunately, with the way these products are advertised and marketed by retail investors in these ETFs, there is a giant disconnect between what is actually occurring vs. what is perceived.

YieldMax initially launched in late 2022 and hasn’t even existed for 4 years yet, yet some claim this is a tool for financial freedom.

The Problem

While there are several issues facing YieldMax and other high-yield ETFs, I would argue the biggest issue comes from a lack of education. This is not the fault of the funds.

NAV Erosion

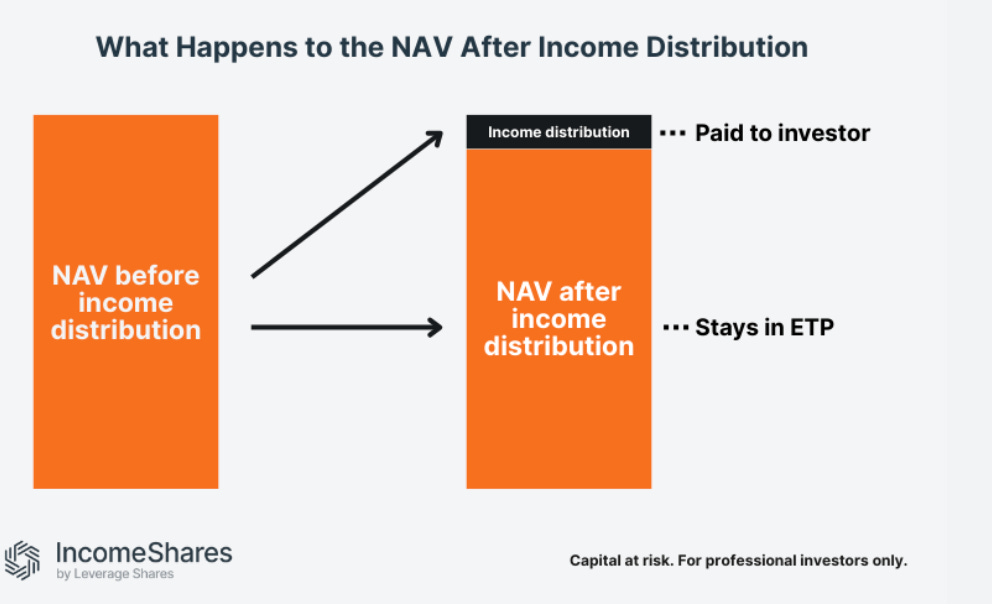

NAV erosion happens when a high-yield fund pays out more cash to investors than it actually earns from its investments. To keep paying that big advertised yield, the fund has to sell off its own assets, which permanently shrinks its overall size and share price.

This creates an illusion of high income/passive income, but over time, it eats away at your initial investment and leaves you with less money and smaller future payouts. The opportunity cost of not focusing on total return is massive, and you would end up with a larger and more tax-friendly return.

Taxes

Since YieldMax generates cash by selling short-term synthetic call options, the IRS classifies this option premium as ordinary income rather than qualified dividends. This means your monthly payouts are taxed at your highest personal marginal tax bracket.

Even if you reinvest the “dividends,” you are effectively giving away 15% to 40% of your compounding power to the IRS every year. Now, if you just bought the actual underlying asset, or better yet the S&P 500, you would get a significantly larger total return, save on taxes, and let your money compound over time instead of paying it away in taxes, management fees, and opportunity cost.

Unfortunately, this is ignored when you get a weekly/monthly payout that feeds a dopamine rush and gives a false sense of passive income.

Fees

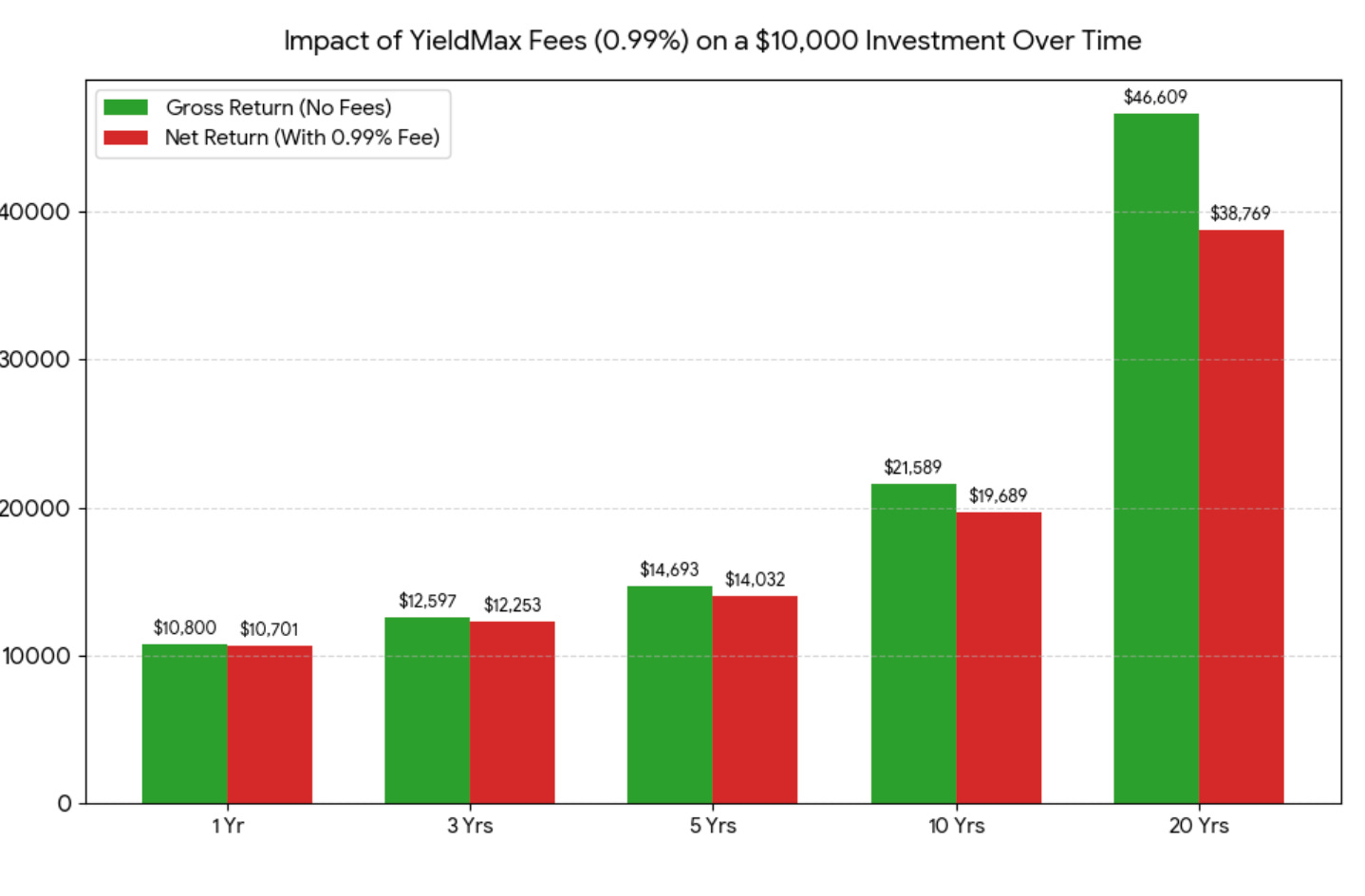

Because these products are actively managed and involve complex daily options trading, their fees are significantly higher than broad-market passive ETFs. Across the entire YieldMax family, the average expense ratio sits at 1.07%.

YieldMax automatically subtracts the annual fee daily from the fund’s net asset value (NAV).

Over a 5-year period, a 0.99% annual fee will eat away roughly 4.5% to 5% of your total potential portfolio value due to the lost power of compounding.

Now, if you actually understood how the options mechanics work, why wouldn’t you just trade the options yourself and save the 1% fee?

Opportunity Cost

The simple fact is there is a massive opportunity cost when you invest in these ETFs. Not only is there significant downside, but also serious tax and compounding disadvantages. These are all shaded by the aspect of having a weekly payout.

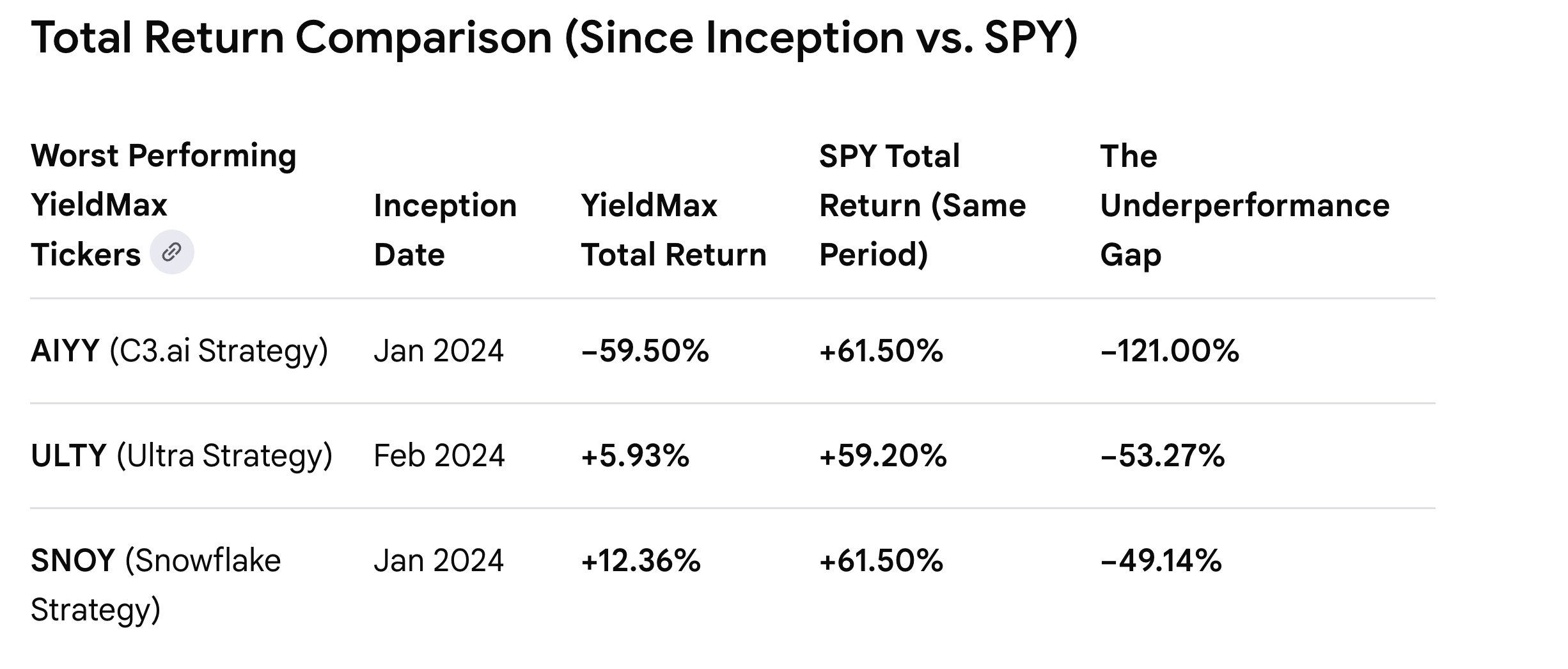

Since inception, if you invested in TSLY, it has underperformed 71.47% of Tesla’s total nominal growth ($4,195 in gains vs. $11,342 in gains) in exchange for turning that growth into highly taxed monthly cash payments.

The S&P 500 gained roughly 97%, while TSLY trailed far behind with a total return of just 42%. This means a $10,000 investment in the S&P 500 grew to nearly $19,750, leaving TSLY investors over $5,500 poorer by comparison.

Since TSLY’s underlying asset is Tesla, you could even make the argument that you got lucky. With other names, some did not.

These ETFs also tend to have insanely high drawdowns. YieldMax ETFs suffer massive drops because they take full blame for a stock’s crash but aren’t allowed to fully enjoy the recovery.

When a stock plummets, the fund plummets with it. However, because the fund sells away its upside profit to generate cash, it misses out on the explosive rallies needed to win that money back. This permanently destroys your initial investment over time.

The Danger

The biggest issue plaguing these funds is misinformation and a lack of education. These funds target the poor and uneducated. They are often spread as a get-rich-quick scheme that can provide serious income used to pay bills, mortgages, etc. Most importantly, it is addictive. Receiving a $200 payout weekly for doing nothing is extremely addictive. Unfortunately, there is no free lunch, and there is a giant opportunity cost.

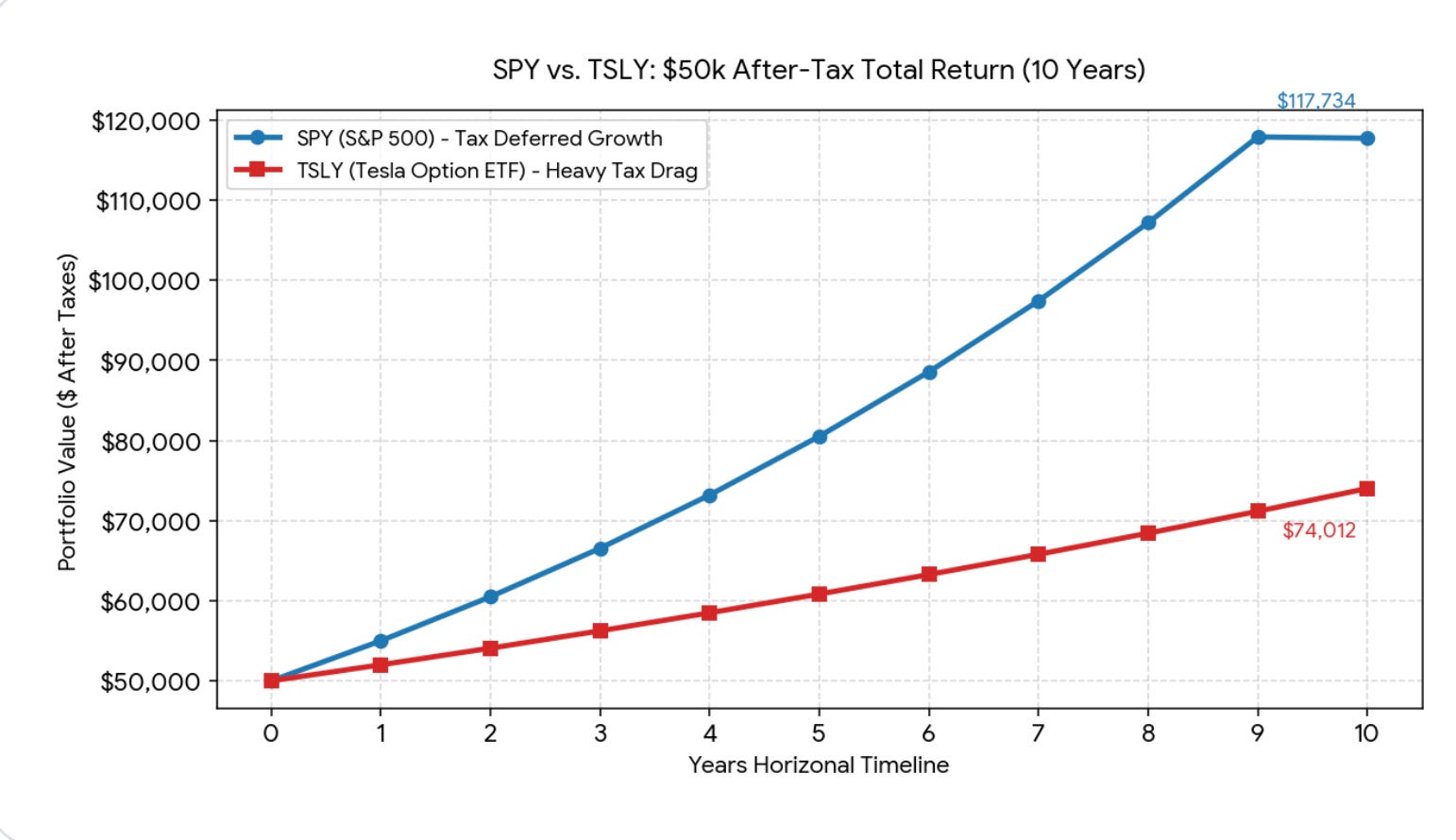

If you invest $50,000 into TSLY right now, you would purchase roughly 1,740 shares (at the current price of $28.73 per share) and receive an estimated $610 per week, which scales up to roughly $2,643 per month.

While a 60%+ forward dividend yield looks incredible on paper, you must expect your actual payouts to fluctuate or drop over time.

If you put that $50,000 into the S&P 500 instead, and are very generous by assuming TSLY can consistently produce a 10% total return, you would still significantly outperform.

What You Can Do Instead

Now, if you truly understand options and how they work, you could trade them on your own, save the 1% fee, and let that money compound instead.

Or, you could simply buy the S&P 500, leave your money untouched to compound tax-efficiently, and then manually sell small portions only when you need cash. Because you held the shares for over a year, your profits would qualify for long-term capital gains tax rates, which can legally drop to 0% if your total income stays below certain federal thresholds.

This gives you complete control over when you are taxed, completely avoiding the forced, high-tax weekly distributions that hurt YieldMax products.

If you are insistent on owning these products, you could at least hold them in a Roth IRA or another tax-advantaged account and reinvest the dividend payouts into the actual underlying asset or the broader market. For example, you could own AMZY and reinvest the payouts into the underlying asset, AMZN.

Recap

At the end of the day, there’s no free lunch in the market. While YieldMax and other high-yield ETFs can produce large weekly or monthly payouts, those payouts come with real tradeoffs that many investors either ignore or simply do not understand. High taxes, capped upside, NAV erosion, management fees, and weaker long-term compounding can all slowly eat away at your returns over time.

That doesn’t automatically make these products “bad,” but they are often marketed in a way that makes the income look safer and more sustainable than it really is. Receiving cash every week feels great psychologically, especially when it looks like passive income that can cover bills or replace a paycheck. But investors should focus on total return and long-term wealth creation, not just the size of a distribution yield.

For most people, consistently buying broad market index funds, minimizing taxes and fees, and letting compounding work over long periods of time will likely produce better results. It may not feel as exciting as getting a weekly payout, but boring investing has historically worked extremely well.

Disclosure: This article is for informational and entertainment purposes only and should not be considered financial, investment, or tax advice. I am not a financial advisor. Investing involves risk, including the loss of principal. Always do your own research and consult a qualified professional before making investment decisions. Any examples or performance figures mentioned are for illustrative purposes only and are not guarantees of future returns.